What Is a Debt Recovery Letter?

A debt recovery letter (sometimes referred to as a debt letter template, debt chasing letter, or late payment letter template) is a written document that formally notifies an individual or business of an outstanding debt. It is typically sent after informal reminders have been ignored and before starting legal proceedings.

In the UK, debt recovery letters often serve as a “Letter Before Action” (LBA) under the Civil Procedure Rules Pre‑Action Protocol for Debt Claims. This protocol requires the creditor to provide the debtor with enough information to understand the debt, respond, and potentially avoid court action.

Debt recovery letters are not just a demand for payment; they are also an opportunity to resolve disputes, open communication, and avoid unnecessary legal costs. They can be used in both business‑to‑business and business‑to‑consumer situations, though consumer debts may have stricter regulatory requirements under UK consumer protection law.

When Should You Use a Debt Recovery Letter?

A debt recovery letter should be used when payment is overdue and previous attempts to secure payment have failed. It is a formal step in the debt recovery process and can be effective in prompting debtors to act before further action is taken.

Here are the main circumstances in which you should use a debt recovery letter.

1. Unpaid Invoices for Goods or Services

When your business delivers goods or completes services and the client fails to pay within the agreed terms, sending a debt recovery letter is often the first formal step toward resolution. This letter should reference the specific invoice number(s), date of issue, and agreed payment terms, while clearly stating the overdue balance.

If your terms of business include interest charges for late payment — for example, under the Late Payment of Commercial Debts (Interest) Act 1998 — this should be included, along with the daily interest rate. You may also wish to attach a copy of the original invoice to remove any doubt or excuse about the debt owed. In many cases, this combination of precision, supporting documents, and a firm deadline is enough to prompt immediate payment.

Expert Tip:

“Attach copies of the original invoice and any prior reminder emails or letters. This shows the debtor you have a clear paper trail, which can reduce disputes and improve your position if the matter reaches court.”

2. Overdue Rent or Tenancy Arrears

For landlords, overdue rent can cause significant financial strain, especially if mortgage payments or property expenses rely on that income. A debt recovery letter for rent arrears should clearly outline the period of non‑payment, the total amount due, and any late fees allowed under the tenancy agreement.

Referencing specific clauses in the tenancy agreement can add legal weight, as can mentioning the potential next steps, such as serving a formal eviction notice under the Housing Act 1988 (for England and Wales) if payment is not received. While the letter should remain professional, it can also invite the tenant to contact you to discuss repayment plans, offering a route to resolution while making it clear that inaction will lead to escalation.

3. Loan or Credit Repayment Defaults

When a borrower defaults on a loan or credit agreement, the creditor’s priority is to re‑establish communication and repayment as quickly as possible. A debt recovery letter in this context should set out the original repayment terms, the missed payment dates, and the total outstanding balance, including any accrued interest or fees.

Where applicable, reference the specific loan agreement clauses that allow you to accelerate repayment or demand full settlement. Including a clear breakdown of charges can prevent disputes and show that the claim is transparent and fair.

For regulated credit agreements, you should also be aware of the rules set out by the Financial Conduct Authority (FCA) to ensure your collection practices are compliant. Offering structured repayment options in the letter alongside a warning of possible legal action can increase the chances of recovering at least part of the debt without lengthy court proceedings.

4. Membership, Subscription, or Service Fee Arrears

Recurring payments such as club memberships, subscription services, or service retainers are often managed by automated billing systems, but when payments fail, a personal and formal approach can be more effective.

A debt recovery letter should outline the missed payment dates, total amount owed, and the impact of non‑payment on service continuation, for example, temporary suspension of access or cancellation of membership benefits.

It’s important to balance firmness with customer retention where possible; offering a reinstatement option upon payment can sometimes recover both the debt and the relationship.

If the membership or service agreement includes late fees, these should be itemised and justified in line with UK consumer law.

5. Before Legal Escalation

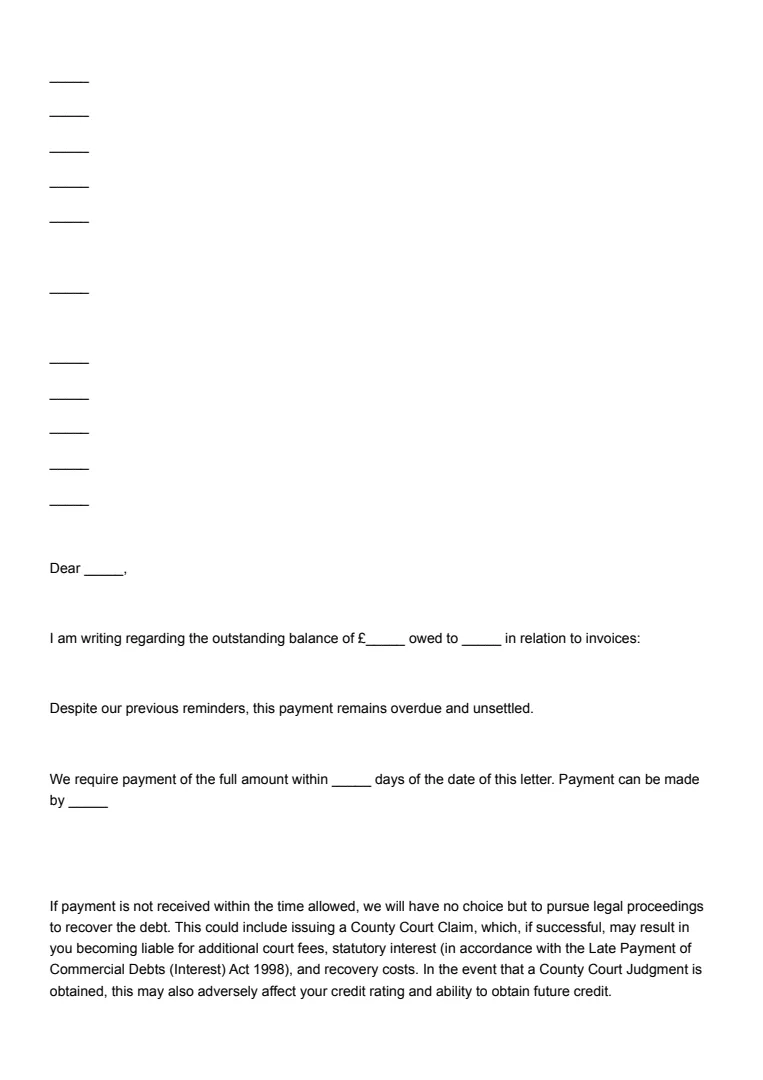

Before beginning legal proceedings, sending a debt recovery letter provides vital evidence that you have attempted to resolve the matter amicably. This is particularly important under the Civil Procedure Rules Pre‑Action Protocol for Debt Claims, which requires creditors to make reasonable efforts to communicate and provide supporting documentation before court action.

The letter should summarise all previous reminders, set a final deadline, and clearly state that legal action will follow if payment is not made. This step not only demonstrates compliance with legal expectations but can also act as a final motivator for the debtor to settle the account, avoiding court fees and potential damage to their credit record.

How to Write a Debt Recovery Letter

An effective debt recovery letter must be clear, factual, and in compliance with UK debt collection laws. It should provide all the necessary details while maintaining a professional and respectful tone.

Here is a step-by-step guide to writing a compliant debt recovery letter or sample letter to creditors for payment arrangements.

Step 1: Identify the Parties

Always begin by clearly identifying both the creditor and debtor with complete legal details. For individuals, this means their full name and residential address as it appears on official records. For companies, use the registered company name, company registration number, and the official registered office address as listed with Companies House.

This removes ambiguity about who is involved in the transaction and ensures the letter has legal credibility if later used in court. Including accurate identification also prevents the debtor from claiming the demand was sent to the wrong person or entity.

Step 2: State the Outstanding Amount and Due Date

List the total amount owed in both numerical and written form (e.g., “£1,250.00 – one thousand two hundred and fifty pounds”) to avoid any misunderstanding. Specify the original due date for payment, along with any reference numbers such as invoice, account, or purchase order numbers that directly link the claim to a documented transaction. If the amount includes interest or late payment charges, break this down clearly.

You can reference the Late Payment of Commercial Debts (Interest) Act 1998, which is explained in detail on the GOV.UK late payment guidance, to support your right to add interest or compensation. This level of transparency reduces disputes and demonstrates that the claim is supported by factual, traceable records.

Step 3: Reference Relevant Agreements

Linking the debt to a specific written agreement adds enforceability and reduces the scope for disagreement. State the exact name and date of the contract, invoice, or service agreement, and highlight the clause or section that sets out payment terms.

If the debt arises from statutory entitlement, such as interest under UK law, mention the legislation explicitly. For consumer debts, review the Pre‑Action Protocol for Debt Claims to ensure the letter contains all mandatory information. Attaching a copy of the relevant agreement or the specific page containing the payment obligation can further strengthen your position.

Step 4: Set a Clear Payment Deadline

Provide a firm, specific deadline for payment rather than vague wording like “immediately” or “as soon as possible.” A typical timeframe is 7–14 days from the date of the letter, although you can adjust this based on the size of the debt, contractual terms, or industry norms. Stating both the date in words and numbers (e.g., “by 14 August 2025”) helps avoid misunderstandings. A clear deadline also supports compliance with the Civil Procedure Rules, which expect creditors to give debtors a reasonable opportunity to pay before escalating.

Expert Tip:

“Always set deadlines in both words and numbers — for example, ‘by 14 August 2025’. This avoids misunderstandings and removes any ambiguity if the letter is reviewed by a court.”

Step 5: Outline Consequences of Non‑Payment

Be upfront about what will happen if payment is not made by the deadline, but keep your wording factual and professional. This could include applying statutory interest, adding late payment charges, initiating proceedings in the county court, or passing the debt to a licensed debt collection agency. If applicable, reference the right to claim costs under legislation or contractual terms.

Clearly outlining consequences helps the debtor understand the seriousness of the matter and the potential financial or reputational risks of ignoring the letter.

Expert Tip:

“Clearly stating your right to claim statutory interest under the Late Payment of Commercial Debts (Interest) Act 1998 often motivates quicker payment, as it shows the debt will cost more the longer it remains unpaid.”

Step 6: Maintain a Professional Tone

The tone of your letter can influence whether the debtor responds positively or defensively. Avoid threats, inflammatory language, or personal remarks, as these can escalate tension or even result in complaints. Use calm, concise, and respectful wording, focusing on the facts and the agreed obligations.

A measured tone helps maintain the possibility of a negotiated settlement and demonstrates to a court that you approached the situation reasonably and in good faith.

Use Legally.io to quickly and easily create your own debt recovery letter, debt letter sample, or letter to creditors template, providing convenience and peace of mind.

What Should a Debt Recovery Letter Contain?

A complete debt recovery letter should include:

- Creditor and debtor information – Full names, addresses, and relevant company details.

- Details of the debt – Amount owed, due date, and the reason for the debt.

- Reference to the agreement – Contract or invoice details supporting the claim.

- Interest and charges – Any applicable late payment interest or additional costs, calculated according to legislation or contract.

- Payment deadline – A specific date by which payment must be made.

- Payment methods – Accepted forms of payment and account details.

- Next steps – What will happen if payment is not made, such as legal action or debt collection.

- Contact details – A named contact and clear instructions for reaching out to discuss the matter.

Legal Tips for Debt Recovery Letters

It’s important to bear these legal tips in mind when creating a sample letter to the debtor requesting payment.

- Follow legal protocols – If the debt falls under the Pre‑Action Protocol for Debt Claims, include all required enclosures, such as a reply form and information sheet.

Expert Tip:

“Where possible, send the letter via recorded delivery and email. This gives you proof of postage and digital delivery, making it harder for the debtor to claim they never received it.”

- Comply with data protection – Ensure you process debtor information in line with UK GDPR guidance from the Information Commissioner’s Office (ICO).

- Be precise with deadlines – Avoid vague wording and use specific dates to ensure clarity.

- Document everything – Keep copies of all correspondence and proof of delivery to support your case if the matter goes to court.

- Adapt for jurisdiction – Processes in Scotland and Northern Ireland differ from those in England and Wales, so adjust the letter accordingly. The GOV.UK guidance on making a court claim for money is a useful reference for the next steps.

Key Takeaways

A debt recovery letter is a vital tool for recovering overdue payments in a professional and legally compliant way.

A strong letter for outstanding payment in the UK provides the debtor with a clear statement of the debt, the deadline for payment, and the consequences of failing to pay.

By following UK legal guidelines, including all necessary details, and keeping a professional tone, you can increase your chances of securing payment without escalating to court.

Legally.io allows you to use a structured, compliant debt collection letter template (UK) that ensures nothing is overlooked and protects your position if further action is needed.